Housing Medallions

Why is Expensive Housing Such a Lucrative Investment?; Big Government Subsidies for Monopolists and the 1%

A popular newsletter genre these days is the business teardown - the writer takes apart a business and really tries to analyze what makes it tick, often with an eye toward whether one should invest in the stock.

Most Americans (66% of American households) are in the business of owning and leasing residential real estate. It just so happens that they usually rent to themselves rather than an outside tenant, but the economics are the same regardless. There is also a plethora of publicly available data about each house online. Why not analyze a business that almost everyone is interested in?

To get into this business, American households routinely enter into a complex and highly leveraged trade where they put 500% of their wealth into a property and fund it by shorting the dollar in a massive way. This is no small industry either; according to the Fed, owner-occupied residential real estate alone is worth $31 trillion at current market value.

I picked a median-priced housing unit in San Francisco to analyze: 333 1st St. #707, a 950 square foot, two bedroom, two bathroom condo in SoMa, close to the Financial District. It’s in a modern glass and steel complex with two buildings, completed in 2004. It’s close to most downtown offices, it’s next to the freeway, and it’s even within walking distance of the baseball stadium. It’s even on sale - it can be yours for the low, low price of $1,149,000, plus closing costs, or about $1,200 per square foot.

Valuing a business is quite simple, whether it is a lessor of residential real estate or a manufacturer of firearms. At least, it is simple in theory. You simply project out all of the cash flow you expect to receive from now through eternity. Discount that back to the present, and that’s how much it is worth.

The challenge is that projecting future cash flow is a matter of being able to predict the future, which is quite hard. Still, there are some methods.

The traditional starting point is to analyze the competitive dynamics of an industry, to predict how much money each player will be able to make in the future. You want to figure out who in the game will have the most scarce asset and thus the most leverage to be able to capture future profits. You can go through a framework like Porter’s Five Forces, looking at barriers to entry, the threat of substitutes, the bargaining power of suppliers and customers, and industry rivalry.

Residential real estate grades badly on almost all of those fronts. There are 140 million housing units in the United States, all competing for renters on price. There are millions of units available at any given time, and millions of units being built every year. There are no brand names, no economies of scale, no network effects, nothing.

Every bit of data about every home is available to consumers on Zillow at any time. If residents start to abandon your city, you have to slash rents to try to keep your unit filled. If residents start coming into your city, homebuilders construct new units to absorb them. The dynamics favor renters.

A recent study by economists Ed Glaeser and Joseph Gyourko confirms this. They find that as of 2013, 84% of cities in the U.S. have median homes which are priced near or below the estimated cost of building a new home in that area.

They also find that inflation-adjusted physical construction costs per square foot have been relatively constant in the U.S. since the 1980s, and land costs have been a minor factor as well, which have kept housing prices from rising too much in most markets.

All of this is consistent with a competitive, commoditized, capital intensive industry that does not generally produce good profits for investors, similar to airlines or auto manufacturers.

How do we reconcile this with the outstanding investment performance of residential housing in a few coastal urban markets? The answer, in my interpretation of Glaeser and Gyourko, is that homeowners in high performing markets form a cartel that prevent developers from producing new homes and pushing rents down.

This cartel is enforced through local governments, which have the power to prevent building through any number of zoning laws and environmental reviews. When there is a surge in housing demand in the region, homeowners can use their market power to capture that income in the form of higher rents and sale prices. By keeping supply close to fixed, it creates a dynamic where for one family to move in, another must leave, and the market rations this by allowing rich families to outbid less rich families for scarce space.

This is famously the case in San Francisco, where homeowners and residents of rent-controlled apartments (who generally do not benefit from new housing either1) enforce a regime that makes building nearly impossible. A 2019 survey cited by Fannie Mae placed the “hard costs” (that is, materials and labor) of a new apartment building in San Francisco at $268 per square foot, not far above other major cities. Later that same year, the San Francisco Chronicle ran a story estimating the all-in costs of a new San Francisco apartment building at $1,116 per square foot, the difference being accounted for by the exorbitant cost of permitted land, as well as the high cost of fees and permits.

The zoning laws and permitting process in San Francisco act as a punitive tax on new development that protects existing homeowners from competition. You will sometimes hear that the high cost of housing in San Francisco is merely a function of the high cost of land, but this is clearly not the case; it is trivial to build hundreds of thousands of square feet of livable space on a small patch of land for less than $500 per square foot, simply by building upward. If housing costs more than $1,000 per square foot throughout most of the city, the scarce factor of production must be permits, not land.

This is similar to the taxicab medallion scheme that artificially restricted the supply of taxicabs in New York and other cities. In New York, the owners of taxicab medallions could lease them to drivers for a steady but growing stream of income. New York taxicab medallions were great investments from their inception in 1937, when they were only $10, through their peak in 2014, when they traded for over $1 million; lease income grew as the city became wealthier and the city government continued to restrict supply, allowing medallion owners to capture the difference.

One way to understand the value of a condominium in San Francisco is that you are really buying a condominium stapled to a medallion. The condominium is not that expensive to build by itself, but it comes with a medallion that confers the right to live in a desirable part of the city. As long as wealthy people want to live in San Francisco, and the city is able to limit the supply of medallions, you will be able to lease or sell the medallion to would-be residents at ever-increasing prices.

The ability for the city to limit the supply of housing medallions is not a given. Citizens are much more concerned about rents than cab fares, and the city can be overruled by the state or federal government. The California legislature has considered and voted down bills in recent years that would allow much more building in San Francisco. Green concerns (suburbs are much harder on the environment than cities) and concerns about affordability make it likely that this issue will continue to come up in future state legislative sessions.2

This issue might eventually make its way to Congress, as well. Matthew Rognlie, then an MIT grad student and now a Northwestern professor, wrote a well-publicized 2015 paper arguing that the growth in inequality in developed countries in recent decades is entirely attributable to higher rents captured by wealthy owners of residential housing, not corporate profits. If income inequality and environmental issues become of interest to the public, the federal government might someday act as well.

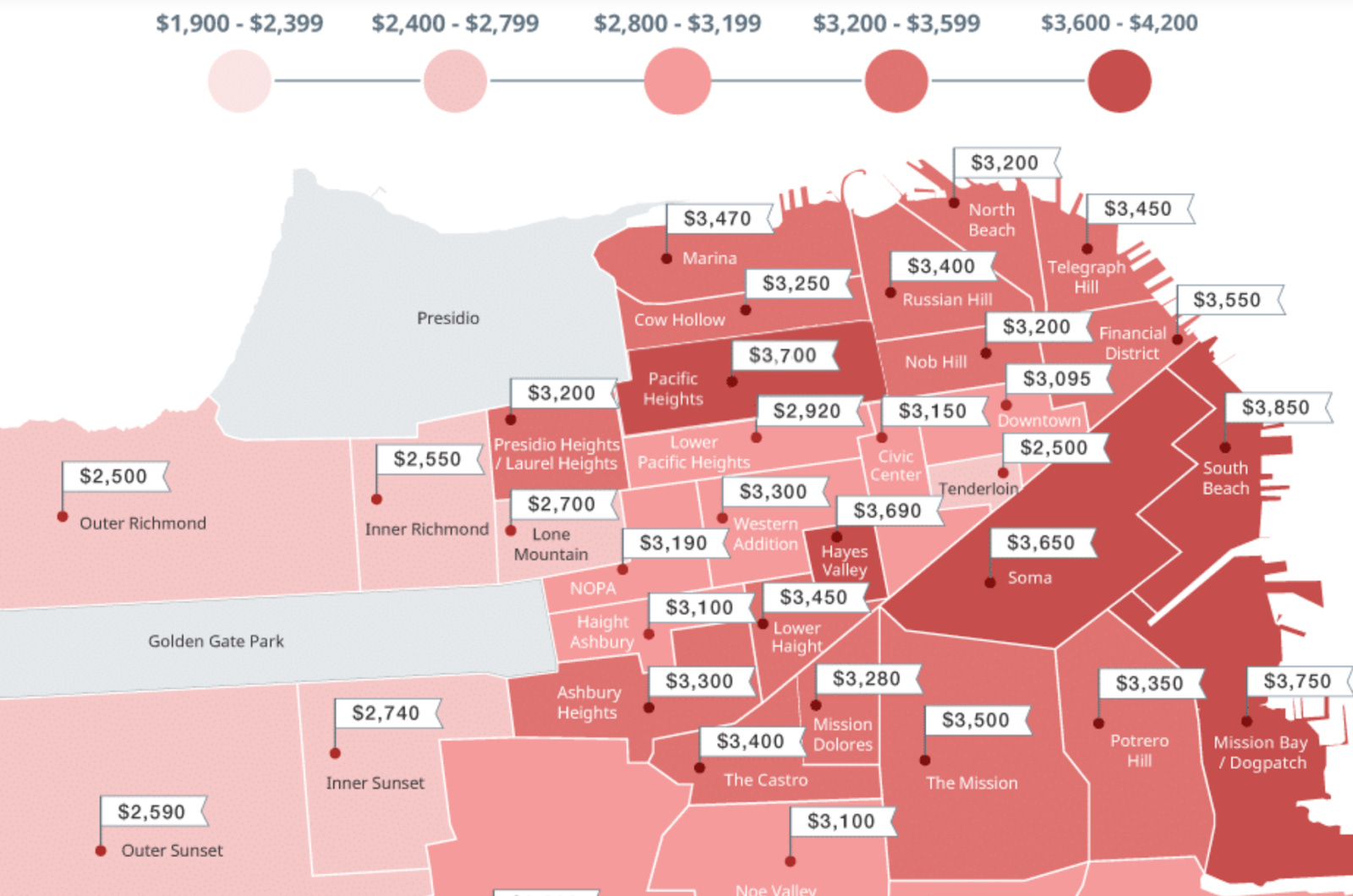

One model of the rental market is that the cost of housing is largely driven by differences in amenities - proximity to transit, access to good schools, safety, and the quality of life of the neighborhood - in short, all of the highlights you see on a Zillow listing. These are clearly important factors, and you can see this clearly if you map rent in San Francisco:

However, the difference in rent between cities is a much bigger factor:

Traditionally, housing prices are closely tied to wages in that city. Unless you are in a city full of retirees or students, the most important factor that determines what people will be willing to pay for rent is what they can earn while living there. In addition, the cost of building a new house depends on the local cost of labor. Rising wages will tend to limit the ability of new housing supply to be created at low prices.

The extreme differential in rents between cities is much higher than would be expected by merely looking at differentials in wages; rents in San Francisco are as much as ten times what they are in other cities in America. This cannot be explained solely by differentials in amenities - San Francisco has access to culture and good weather, but so do many other much cheaper cities. Also, most of these cheaper cities lack San Francisco’s issues with safety and human feces on the sidewalk. The main factor must be the housing medallion system we identified earlier.

The question we have to ask is, why do companies in competitive markets continue to employ people in such an expensive city? In an earlier edition, we examined the concept of agglomeration effects, which are important in deterring companies in a given industry from relocating. The workers want to be physically located where the companies are, and vice versa, and the companies also want to be located near important customers (such as other tech companies) and suppliers (such as venture capitalists). Physical proximity is also important for the transfer of knowledge between workers and between firms. To be productive, everyone clusters together.

By forming a cartel to create artificial scarcity in a normally abundant factor of production - housing - homeowners in San Francisco have been able to put themselves in a position to tax and capture a large share of the benefits of innovation, at the expense of investors,3 taxpayers, and workers (from construction workers who don’t have jobs to rank and file4 employees).

This raises the question of sustainability. Homeowners are taxing local companies indirectly - their workers receive higher wages, which get passed on in the form of rents. The companies want to avoid paying this steep tax, if only to stay competitive.

One possible explanation is that there are short-term effects and long-term effects. The classic example is oil prices - when there is a big spike in oil prices, it causes a big short term spike in gas prices, but over the longer term, people trade in their gas guzzlers for hybrid cars, and demand fades.

In the tech industry, startups are willing to spend aggressively up front to capture market share in a new industry. They expect it to pay off later if the customer base they acquire is sticky, or if they generate network effects or economies of scale that cannot be matched by other companies. It is rational for them to pay higher rent initially, and to seek to move their employee base later. The Wall Street Journal describes this process in a profile of a major software company buyout fund, Vista Equity:5

Former employees say cost cutting is critical to Vista’s model. Some of the companies Vista takes over are located in markets with a high cost of living, such as Southern California or New York City. To tamp down wages and other costs, Vista will relocate part or all of the company to a less-expensive city such as Dallas. Many employees won’t make the move, allowing Vista to hire cheaper replacements. Vista often keeps a company’s headquarters in place and encourages it to expand in lower-cost markets.

The most valuable tech company based in San Francisco, Salesforce, announced last week that most of their employees would permanently be allowed to work remotely, coming into the office at most one to two days a week. The article notes that other major San Francisco tech companies have also already announced a permanent move to partial or total remote work. Total remote work would allow employees to move out of California entirely, but even partial remote work would open up the possibility of moving far away and suffering a long commute one or two days a week.

If I had to make a prediction, it’s that the biggest risk to housing prices in San Francisco (for an owner) is not the prospect of increased supply from housing reform, which in any case would take many years. It is the risk of companies leveraging technology to move or or work remotely. It is similar to what caused the taxicab medallion market to crash - technology enabled a competitive solution, and the government declined to intervene.

Ok, back to our San Francisco condo. The current best offered rent on Craigslist for a similar unit in the building is $3,700 a month. (By comparison, the rent for a similar unit back when I lived there in 2007 was $4,000 per month!) It does seem like similar units were going for more like $5,500 per month pre-pandemic, so we can also model that scenario as a possible longer-term equilibrium, if we believe San Francisco is going to bounce back.

As a point of comparison, I also show Equity Residential (EQR), a $25 billion publicly-traded real estate investment trust that owns a diversified portfolio of apartment complexes in San Francisco (20% of their portfolio) and other major similar supply restricted cities and suburbs. I tried to show your portion of the 2019 income statement if you bought just enough shares to create the same economic exposure to high end urban real estate through EQR as you would get by buying a San Francisco condo.

It is useful to look at a publicly-traded comparable to any business you try to analyze - you can understand your business better, you understand your opportunity cost better, and at the end of the day you might decide it’s a better bet to simply buy the stock of the comparable company.6

The pandemic has been really bad for downtown big city real estate. Rents are down 20% or more, but expenses are fixed, so it’s an even bigger impact on property income. To buy now in San Francisco, you are making a big bet that there will be a strong recovery in rent in the coming years.

EQR has the benefit of having a big portfolio of apartments in the suburbs of big cities as well, which have not performed as badly. Still, the stock is down 23% over the last year, while the S&P is up 16%. You can indeed buy EQR at a much more attractive cap rate (a measure of valuation that excludes debt) than the condo we picked in San Francisco, even assuming a big bounceback in San Francisco rent. However, EQR does not carry much debt (about a quarter of total capital), while you can buy the condo for about 30% down and still qualify for a conforming mortgage, so you get a lot more house per dollar of cash invested if you buy a condo.

The biggest difference between buying a condo and buying stock in EQR is the cost of buying and selling a small single property - realtor commission, title insurance, and so on. I estimate that cost at nearly $70,000. I estimate the cost of buying the equivalent value of EQR through Robinhood to be about $16 in payments for order flow. Guess which one we had Congressional hearings about this week? If you ever wondered why the National Association of Realtors is the biggest lobbying group in DC, wonder no more.

The most interesting item to me is the “Tax Subsidy” line I highlighted. Normally, if you own an investment, you pay taxes on the income generated, at least on your personal tax return, but usually also at the corporate level too. But if you own a property and live in it, that investment is suddenly no longer subject to tax at all. You owe absolutely zero. It’s an incredible tax break, one of the most generous ones in America, and it swings the pendulum heavily toward property ownership for wealthy households in higher tax brackets.

You can understand it by thinking through this example. If you sell the condo to EQR, the shareholders of EQR have to pay tax on the rental income generated each year (albeit with a small tax break). If you buy it back and live in it, the rental income is suddenly not taxable at all. The property has not changed at all, it’s just a function of whether the owner and the renter are the same person. It’s taxed if EQR owns it and rents it out, it’s not taxed if you own it and live in it.

This is known as the tax break on imputed rental income. In many other developed countries, such as the Netherlands, this income is taxed. Keep in mind this tax break does almost nothing for homeowners in lower income tax brackets - it is a huge tax break squarely targeted at the rich, particularly the rich in high tax, high rent states, who have expensive houses.

Big tax breaks targeted at homeowners are already a bit suspect, since homeowners as a group are already wealthier than the renters who have to fund those tax breaks. If we want to incentivize homeownership, why don’t we just send a flat check to all homeowners, regardless of income? And even then, why should the cost burden fall on people who cannot afford a down payment and must rent?

Huge tax breaks targeted at super wealthy owners of expensive land and houses are somewhat absurd. In this model, taxpayers are effectively cutting a check of over $17,000 each year to someone who owns a million dollar condo, just for the tax break on imputed rental income. Then on top of that, taxpayers cut another $9,000 check for the deduction on interest.7 And in California, on top of that, we have Prop 13.

But that’s not all. Usually, when people advocate for a tax cut on investment income, the stated logic is that it will incentivize investment, which is good for the economy, and the benefits will trickle down, creating employment and wealth. But we have just seen that an investment in super expensive urban housing is actually mostly the purchase of a medallion! And the medallion is valuable only because the owners are able to restrict investment in the economy.

Think about it. By giving big tax breaks to people who own land in high cost cities, and who have the power to block new housing, we are just increasing the return to blocking investment in new housing in America. If cities are successful in blocking new construction, rents will rise and the more valuable the property becomes.89 Then when they go to sell their appreciated property afterwards, the first $500,000 of capital gains are tax free as well, which is another tax break worth up to $200,000!

It’s one thing to allow cities and households to block new housing. It’s quite another to pay them to block new housing, destroy construction jobs, and lower the standard of living for the rest of the country.

“Halt the exemption on imputed rent for residential housing which has an appraised value of over $500 per square foot, unless it is in a municipality that is growing housing supply by over 2% per year” doesn’t have a catchy ring to it, but we can workshop it.10 Maybe there is a compromise - you can block new housing, or you can have a tax break on expensive housing, but you can’t have both.

Anyway, that is not investment advice, just a bit of commentary on public policy. I do not provide investment advice here, but any time you can invest $300,000 and get yourself a $26,000 check every year from the government for doing so, and then another tax break worth up to $200,000 when you cash out, you should seriously look into it. In a city like San Francisco, where the homeownership rate is only 37%, the market price for housing investment is probably partially determined by taxable owners like EQR, so we shouldn’t expect this to always be fully captured in the price.

If you ever wondered why it’s so common to build wealth through investment in expensive residential housing, you should consider that a relatively small equity investment confers the right to get an annual check from the government equivalent to the per capita GDP of Taiwan. It’s hard to screw up an investment when you have that kind of tailwind. (But definitely possible - do your homework! This is not investment advice!)

So, to recap, when you buy a condo in San Francisco, you are really getting a condo stapled to a medallion stapled to a fat government subsidy. You can work out the value and the risks associated with each factor and come to your own conclusions about whether to invest.

The other side of the trade, where you short the dollar, is worth a comment as well. The 30 year fixed rate mortgage is a bit of a strange instrument, if you think about it, but in the current low rate environment, it is an attractive one. If interest rates rise, the value of your condo/medallion/tax asset will decline, but so too will the value of the debt you took on to buy it. Also, if inflation rises, it will be a windfall in real terms; your real estate will be worth the same, but your debt will have been devalued.

Even if inflation doesn’t rise, you should do well. The 30-year carries a 2.81% interest rate, which costs only 1.65% after tax in California if you are in a high enough tax bracket to afford a house; inflation expectations over the next ten years are around 2% annually, meaning you can expect to gain more each year from the devaluation of the principal you owe than you spend on interest.

There is a lot more we could discuss in relation to residential housing - we haven’t even touched on the diversification effect (or lack thereof) from buying a house, the psychic and status reward of owning a house (as opposed to stock in a REIT), and the positive and negative effects of incentivizing people to stay in one city. This is just a starting point.

One last observation: The residential real estate business is actually not that special. You can apply the framework you use to analyze an investment in equity in a residential property to analyze an investment in the equity of a major company. The same themes recur constantly - big tech companies also benefit from massive tax breaks, regulatory barriers to new competitors, and threats from regulation and new technology. But we can save that for a later edition!

One issue is that new housing can result in the destruction of rent-controlled units, even when there are rules against it. Even more generally, higher rents tend to mean higher wages, as private businesses have to compensate their employees for the higher cost of living. Most people make much more than they spend on non-housing costs, so as long as you have a job, you should selfishly be against new housing if you have a rent-controlled apartment, even in the unlikely case you don’t mind change in your neighborhood.

John Myers proposes a clever idea to break the cartel by permitting the residents of each street in a city to determine their own zoning. This is probably politically more palatable than allowing a building free-for-all but would also probably still have the desired effect by allowing players to more easily defect from the cartel and build more housing.

Interestingly, theory predicts that any subsidies the government tries to funnel into the system to promote innovation - R&D subsidies and tax breaks on investment, for example - will largely get captured by the people who control the scarce factor of production, in this case housing.

This will not affect the highest paid employees as much, as they are so well remunerated that they are not likely to spend a significant portion of their paycheck on housing.

It recently came to light that the founder of the firm was allegedly involved in the largest tax evasion case in U.S. history - another way to cut costs, apparently.

You can often learn everything you need to know about an industry in the first couple of pages of the annual report. From the EQR 2019 annual report: “We seek …[markets with]...higher barriers to entry where, because of land scarcity or government regulation, it is typically more difficult or costly to build new apartment properties, creating limits on new supply”.

In fairness, the way the current system is structured, being able to deduct interest as an expense is normal, if you pay taxes on your income. Anyway, there is a good argument that interest should not be deductible as an expense for anyone, businesses included, so I include it here.

A key part of the model here is that higher rents largely get covered by higher wages, in most cases. Businesses have to compensate workers more in high cost cities. Owning a house hedges you against increased rent, which is important for a retiree who does not want to have to move, but most people are workers, so workers that own a house get higher wages without having to pay higher rent, pocketing the difference tax-free.

Many economists throughout history, most famously Henry George, have advocated a land value tax as being the most efficient and equitable tax, as it is progressive, it encourages development, and it does not distort supply (since the supply of land is fixed anyway). Somehow in America we have managed to do the opposite and made land the only investment which is effectively mostly tax exempt (particularly in California because of Prop 13), with the predictable outcome of discouraging investment and promoting inequality.

Commenting about 10 months after the article was written ...

I love all your articles. I started with the one on Cartels and am rabbit-holing my way through the others. Kudos and thanks for the great work!

That said ...

I don't buy the need to tax imputed rent as a panacea for bloated housing costs - a mortgage, which most owners have, is rarely less financially onerous than paying rent. Simply eliminating the deduction on mortgage interest will go a long way to eliminating the distortion between renting and owning.

Of course, if you're going to go after that mortgage interest deduction, you need to also whack corporates ability to deduct interest, or you will see homeowners turn into real estate investors by forming corporations and buying their single-family homes that way instead.

There will also likely be a huge re-adjustment in the corporate credit markets (and a massive tremor in the LBO business) if ever the corporate deduction on interest is removed, but once the adjustment is done, all will be well and Wall Street will continue to thrive, boom and periodically go (almost) bust and be bailed out.

As for eliminating distortions imposed by zoning, etc., good luck on that (Federalism, etc.) - one just has to let competitive dynamics between geos to attract business to locate in their areas do the trick, aided by the continuing advance (one hopes) of telecommuting options. That's helping the likes of Austin right now, but it hasn't as yet started to hurt NYC and SFO. As yet ...

This is great writing - cogent and unique.

Re your prediction in the article - I have to wonder if there's a coming backlash to remote work. I've been remote for a year now, and it's incredibly difficult to communicate complex ideas over zoom. I feel like a lot of roles in product and engineering will be push back to in person, especially for more senior employees.